Whether you have your own business or work for an employer, protecting your income stream from an illness or injury that will prevent you from working should be a priority.

According to the Social Security Administration, more than 25% of 20-year-olds will experience some form of disability before they reach retirement.1 Whether it’s a ski trip gone wrong, an illness, or a necessary surgery like a knee replacement, disability insurance can help replace income while you recover.

Disability insurance is designed to pay out a portion of your income if you were unable to work due to illness or injury, and in this article, we break down how this coverage works and what you need to know about it.

The Purpose of Disability Insurance

You may have heard it referred to as income protection insurance or simply “DI,” but disability insurance is insurance against the risk of being unable to work.

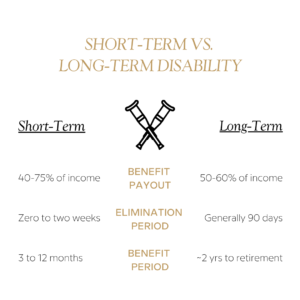

And even though it’s a basic form of insurance, it’s reported that only one in three Americans have the appropriate coverage.2 Typical costs vary, but you could expect to spend 1-3% of annual income in premiums for a policy that can replace anywhere from 40-75% of income. The benefits paid out are generally tax-free unless the policy was paid for with pre-tax dollars.

The two factors that play the most significant role in the cost are the length of the elimination period and the benefit period. The elimination period is the window of time that you must wait before receiving benefits. The benefit period is how long the benefits will continue to be paid after being issued.

Types of Coverage & Where to Purchase

There are generally two forms of disability insurance – short-term and long-term. While they both replace a portion of income, long-term coverage typically pays out less monthly because the coverage extends for a longer period. Short-term coverage may pay out higher benefits, but the benefits don’t last as long, typically less than one year. However, short-term coverage usually means a shorter waiting period after experiencing a disability before the benefits start being paid out.

Two of the most common ways to purchase a policy are through your employer, insurance firm, or broker. Many employers offer partial or fully paid disability insurance. However, if they don’t cover any costs, you may still be able to purchase a policy through them at a discounted group rate. If you’re self-employed or your employer doesn’t offer disability, you can buy an individual plan from a standard insurance company.

To qualify for a policy, self-employed individuals may have to show tax returns and two years of consistent income. Also, an individual policy would only cover income drawn from the business, not income the business needs to continue running. Just like standard disability insurance, business overhead expense (BOE) insurance would help cover business expenses if an injury or illness stops you from working.

A few factors that will affect the monthly premiums and the ability to get an individual policy include:

• Age

• Gender

• Health & past conditions

• Income

• Occupation

What to Keep In Mind

Overall, the most important thing to keep in mind when deciding on a policy is how much of your income you would need to replace your current expenses if you were unable to work. This helps determine the appropriate coverage, which also plays a role in the overall cost.

Also, think about how long you may need the benefits to last. If you have a working spouse, short-term coverage could be sufficient to bridge a few months of income. Or in situations where your income is the only source of funds, it may make sense to purchase a long-term policy that can last all the way to retirement, even though the monthly premiums are generally higher. Whichever route you decide to take, ensure that you understand the cost of the premiums and the length of both the elimination and benefit periods.

While the term ‘disability’ sounds heavy, it can mean many different things in the context of disability insurance. It could be as serious as paralysis or a lesser disability such as a back injury or illness. Or it could just cover the recovery time for necessary surgery, such as a knee or hip replacement. If an illness or injury hinders you from working, it’s generally considered a disability to be covered by the policy.

The Takeaway

It’s reported that only 40% of households in the U.S. have enough savings to cover at least three months of expenses.3 While we usually have insurance for hard assets such as our cars and homes, a soft asset that gets overlooked is the ability to create income. In a busy life, it’s easy to put off getting a policy – and then it’s too late.

1. SSA. Social Security Basic Facts. 2021. Social Security Administration.

2. Schott, Fred. How Many Working Americans Have Adequate Disability Coverage? April 26, 2018. Council for Disability Awareness.

3. Bhutta, Neal. Lisa Dettling. Money in the Bank? Assessing Families’ Liquid Savings using the Survey of Consumer Finances. November 19, 2018. Federal Reserve.

This work is powered by Seven Group under the Terms of Service and may be a derivative of the original. More information can be found here.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA